|

|

|

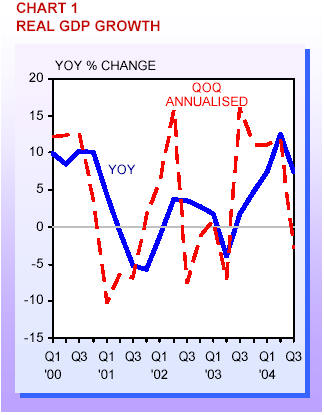

Growth of the Singapore economy

eased to 7.5% in 3Q04, from 12.5% in 2Q04. The growth momentum, on an

annualised quarter-on-quarter basis, declined by 3.0%, after the 11.9% rise in

2Q04.

See

Chart 1 |

|

Sources of Growth |

|

Total demand rose by 18.7% in 3Q04, compared with

a 22.5% gain in 2Q04. This reflected a slower growth of both external and

domestic demand.

See

Chart 2 |

|

External demand grew by 21.4% in the quarter, down

from 25.8% in 2Q04, mainly on slowing electronics exports. Services exports

also grew slower in 3Q04, particularly in the travel and transportation

services sectors. |

|

This largely reflected the post-SARS recovery of

activities in the year-ago period. The higher base effect also showed up in

the growth of domestic demand, which slowed to 10.3% in 3Q04 compared with

13.6% a quarter earlier. Apart from slower growth in private consumption, this

also reflected declining public sector |

|

Sectoral Performance |

|

With the exception of the construction sector, all

other major economic sectors registered positive growth in 3Q04. The pace of

growth of all sectors, however, has moderated from the second quarter (see

Annex). |

|

THE MANUFACTURING SECTOR registered growth of

11.5% during 3Q04, moderating from the 20.7% growth in the previous quarter.

This slowdown was mainly due to lower-than-expected biomedical output.

See

Chart 3 |

|

The electronics cluster, however, expanded at a

faster rate of 26.4%, following the 25.3% growth in 2Q04, on the back of

strong demand for semiconductors and computer peripherals. |

|

Growth of output in the chemicals cluster also

accelerated to 11.1% in 3Q04, compared with the 5.9% gain recorded in 2Q04. |

|

THE CONSTRUCTION SECTOR contracted further by

10.9% in 3Q04, following the 5.9% contraction in the quarter earlier.

See

Chart 4 |

|

There was a weakening in both public and private

sector construction activities. Public sector certified payments declined by

15.1%, with all segments recording slower activity. |

|

Similarly, private sector construction work also

receded by 13.1%, with declines in all but the institutional segment. Total

contracts awarded continued its downward slide, declining by 22.9%, following

the fall of 13.9% registered in 2Q04. |

|

THE WHOLESALE AND RETAIL TRADE SECTOR expanded by

15.7% in 3Q04, easing from the 18.9% rate of growth in 2Q04.

See

Chart 5 |

|

Entrepot trade remained robust, with non-oil

re-exports growing by 24.9%. Domestic trade moderated slightly, as growth of

retail sales eased to 10.1%, from a 14.1% increase in 2Q04. |

|

Supported by continued strong sales of wearing

apparel and footwear, retail sales excluding motor vehicles increased by 7.7%,

after a 9.9% gain in the earlier quarter. |

|

THE HOTELS AND RESTAURANTS SECTOR registered a

gain of 6.7% in output during 3Q04, compared to the strong 38.9% growth

recorded in 2Q04.

See

Chart 6 |

|

The slower rate of growth mainly reflected the

post-SARS recovery of activities in 3Q03. Compared to 3Q02, however, the

sector registered a decline of 2.1%. This reflected lower revenue from cess-paying

establishments and the decline in hotel room rates from levels recorded in

3Q02. |

|

Partly offsetting the impact of these factors,

visitor arrivals rose by 13.3%, compared to 3Q02, while the average occupancy

rate for gazetted hotels rose to 83.1 per cent, a 9.5 percentage-point

increase from 3Q02. Hotel room revenue also reached $248 million, a 1.8%

increase compared to the same period two years ago. |

|

GROWTH IN THE TRANSPORT AND COMMUNICATIONS SECTOR

was also dampened by the higher base effect.

See

Chart 7 |

|

In 3Q04, the sector grew by 8.9%, compared with

the 18.9% growth in the earlier quarter. The slowdown mainly reflected weaker

growth in the air transport segment. |

|

Growth of the sea transport segment was little

changed and sea cargo handled grew by 17.1%, an improvement over the 13.9%

recorded in 2Q04. |

|

The communications segment also continued its

expansion. During 3Q04, IDD call duration rose strongly, while mobile phone

and broadband subscriptions also registered gains. |

|

THE FINANCIAL SERVICES SECTOR grew by 4.1% in

3Q04, moderating from 5.3% in the previous quarter. Several key segments of

the sector continued to expand in the third quarter.

See

Chart 8 |

|

Trading activity in the foreign exchange market

remained robust and fund management activities continued to improve,

reflecting the strengthening of investor confidence. |

|

The turnaround in insurance-related activities was

also sustained in 3Q04. In comparison, activity in the domestic stock market

remained lacklustre and banking activities were generally slower, due mainly

to weaker earnings from fees and commissions. |

|

THE BUSINESS SERVICES SECTOR expanded by 2.2% in

3Q04, easing from the 3.5% gain in 2Q04.

See

Chart 9 |

|

This was largely due to the slowing of growth in

the real estate segment, the largest segment in the sector. |

|

However, the IT and related services segment

continued to grow strongly. Professional services – such as accounting and

legal services – also registered higher growth rates in 3Q04. |

|

More..... |

|

Source:

Ministry of Trade and Industry Press

Release 17 Nov 2004 |